No AI was used in the creation of this post. Enjoy!

Table of Contents

View Table Of Contents Here

Key Takeaways

- Mortgage protection takes care of the mortgage in case you pass away. However, it’s greatly evolved over the years.

- Nowadays, the money goes to you and your family, and you may be able to qualify for additional benefits.

- If challenges come our way, we’re not afraid of coming up with creative solutions to protect you and your family.

Congratulations, you closed on your home! Or, you re-financed. Now what?

Buying a home is a serious commitment, no matter how many years your term lasts. That’s why it’s important to protect it, too. If one or both of the main breadwinner(s) suddenly pass(es) away, the surviving family can find themselves unexpectedly burdened by immense financial stress.

Mortgage protection has evolved over the past few decades. Traditionally, mortgage protection is offered by your lender. Nowadays, better options are likely available for you. We also use creative strategies for those who may have trouble qualifying for traditional life insurance products. Let’s dive into mortgage protection, and how it can protect you and your family!

What Is Mortgage Protection?

Mortgage Protection Insurance (MPI) is a certain kind of insurance policy. Traditionally, it covers your mortgage in case one or both spouses pass away. Also, it often follows your mortgage as you pay on it.

What does that mean?

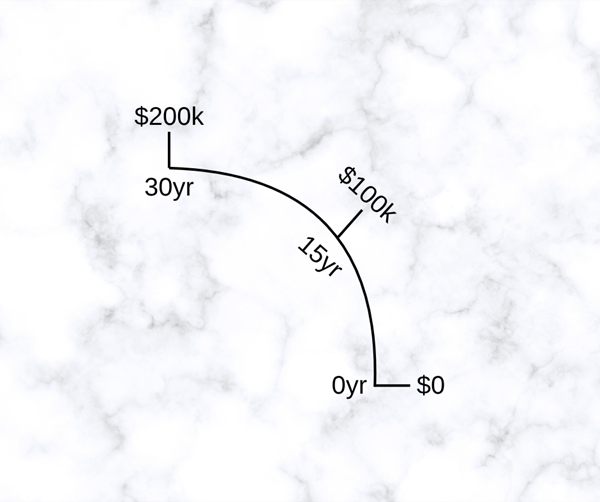

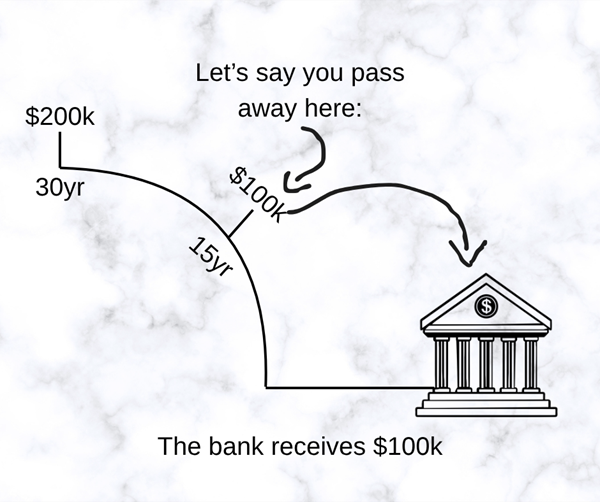

Let’s say you just closed on your home, and your mortgage is $200k (with everything put together). Let’s also suggest you’re the main breadwinner of the household. If you pass away with $100k left on the mortgage, $100k will be paid directly to your bank. These payments can either happen periodically, or in one lump sum.

Some traditional MPI policies allow you to add extra benefits (called “riders”) if you become disabled, lose your job, etc. One upside of traditional MPI is a medical exam usually isn’t required to qualify for a policy. However, guaranteed acceptance may also come at a price – that is, an increased premium.

Likely, your premium won’t decrease along with your coverage.

MPI & PMI (& MIP?)

PMI (Private Mortgage Insurance) isn’t the same as MPI (Mortgage Protection Insurance), but the acronyms can be confusing.

PMI protects your lender in case a foreclosure happens due to non-payment.

Usually, you’re required to pay for PMI if your down payment is less than 20% (and if you applied for a standard loan). However, you can usually cancel PMI when your equity reaches 20% or higher.

While we’re on the topic – MPI is not the same as MIP (Mortgage Insurance Premium). If you take out a loan that’s backed by the Federal Housing Administration, you’re required to pay an MIP. You don’t need as high of a down payment (or credit score) to qualify for these kinds of loans. So, they like playing it safe by requiring you to pay an MIP, just in case you default.

For our purposes today, however, it typically doesn’t matter which kind of loan you have.

How Much Does MPI Cost?

If you put “mortgage protection quote” into your search bar, you’ll notice something – a lot of these websites don’t ask for any of the medical information they need to form your “down-to-earth” quote.

This means that, even if you get a quote sent to your inbox, it’s probably an estimate.

I frequently ran into this problem when I worked in the auto insurance industry – people would be shown estimated premiums, and I’d ask for all of the information I needed to form an actual quote. Often enough, I found incidents on their record that increased the price of the estimate. For example, if you had 2 accidents and 3 speeding tickets in the past 5-or-so years… Sorry, that $58/mo isn’t going to work after all. Maybe you’ve experienced this before as well.

That’s why it can be difficult to answer this question. Each and every quote is based on your individual situation, and is tailored to your specific needs. It’s impossible to offer a real answer without asking for everything we need to know.

That’s what makes our quoting process so different. We’re HIPAA-compliant, so we’re allowed to be very detailed and thorough with the questions we ask. We can obtain and store sensitive medical (and mortgage) information because we follow certain procedures that other people may or may not follow.

Even if you submit your information online, we still call you to verify that the information is correct, and to set an appointment. Normally, we show your personalized quotes during the appointment.

While this may sound more cumbersome on the surface (who doesn’t like getting a bunch of quotes online, after all), we’re dedicated to giving you actual quotes for products that you actually need – and that takes time and effort. Quality over quantity, as they say.

Generally, though, we aim to form solutions that cost anywhere from 1.5%-2% of your yearly salary. For example, if you make $50,000/yr, that’s anywhere from $750 to $1,000 per year. That comes out to $62.50-$83.34 (rounded up) per month.

(Visit this website to find out what that means for you.)

In our experience, most people can afford 1.5%-2.5% of their salary in premiums, sometimes more, sometimes less. Sometimes we have to get creative, which we’ll talk about in a bit.

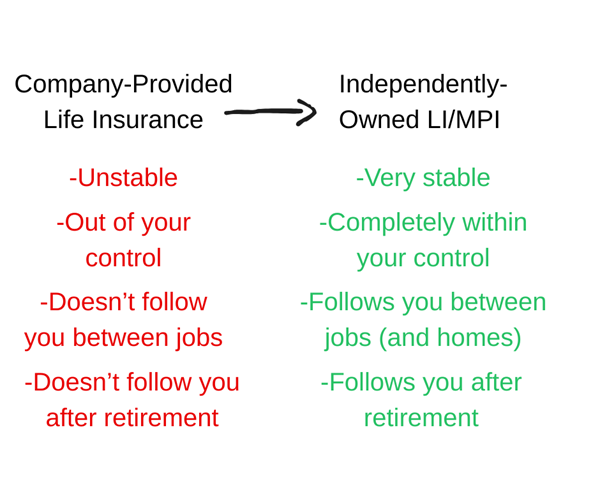

Mortgage Protection Has Evolved

As you can imagine, people weren’t too happy about the payout going to their bank. What about funeral expenses? Unexpected expenses? The loss of their spouse’s income? The time and ability to perform the many legal requirements that arise after the death of a loved one? And possibly more…

All while grieving the loss of your spouse.

So, something interesting happened – the life insurance companies stepped up and said, “We can do better. We can offer better mortgage protection products than what the banks offer.”

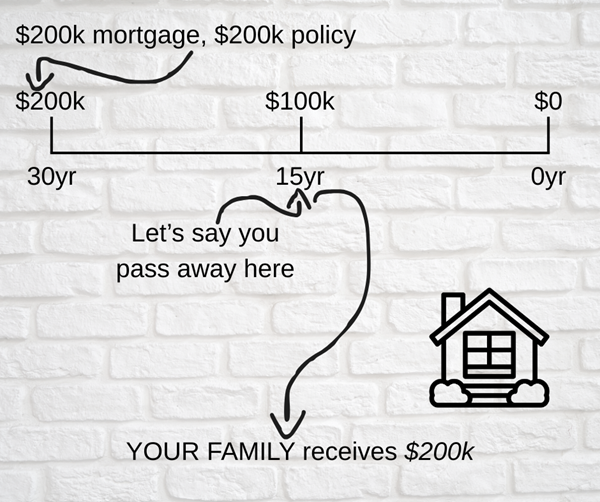

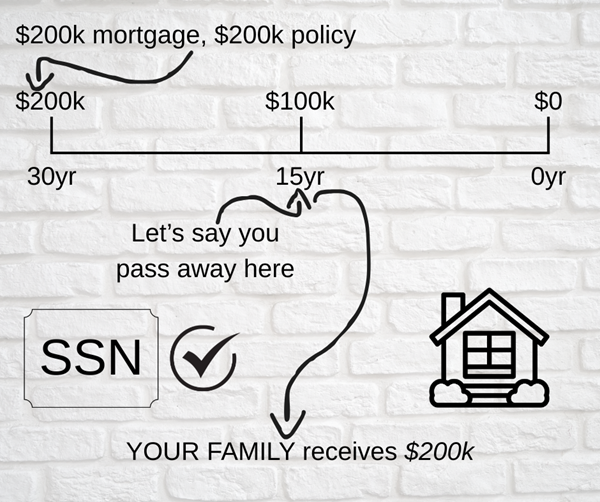

And so they did. This is how it works nowadays, assuming a $200k mortgage with a $200k MPI policy:

Let’s compare the two side-by-side:

Instead of your policy being tied to your home, it’s tied to your SSN. If you move, it moves with you. And of course, you/your family receive(s) the money instead of the bank.

If your mortgage starts at $200k, and you pass away when the mortgage is $100k, what happens to the other $100k? The insurance company re-possesses it! Just kidding. After your family pays off the home (and generally takes care of business), they keep the rest of the money.

That’s the power of insurance company-based mortgage protection policies. This is what MPI is in the modern day.

“Great,” you may be thinking, “but this sounds a lot like life insurance.” And you’re right – this kind of mortgage protection is a lot like life insurance. There are a few key differences, though.

The first (and most obvious) is that you need a mortgage to qualify for MPI products. Some companies are a bit more lenient – if you’ve taken out a mortgage in the past, you can still qualify for some of their MPI products, even if you don’t have one now.

The second is you will almost certainly enjoy reduced underwriting guidelines. While simplified life insurance has existed for a while, the idea is that since you have a mortgage, you go through less underwriting while (on average) qualifying for more options at higher age ranges than if you were applying for a life insurance policy. Same goes for any and all living benefits.

If you’re applying for an incredible amount of coverage ($500k-$1m+, depending on the company and your situation), you may still have to jump through some hoops.

The third and most interesting difference is what we like to call, “Mortgage Payment Protection,” or “Critical Period Coverage.” We usually explore other options first, but it definitely has its place when integrated properly. We’ll talk more about it a bit later on.

Who Needs Mortgage Protection Insurance?

The numbers are there. The studies are there. But, if I’m being honest, that’s not the direction I want to go in. I’ll simply leave this here if you want to read it. This info-graphic is for life insurance, but life insurance statistics are similar to insurance company-based MPI policy statistics.

Instead, I want to ask you a question. Assuming you reading this are the breadwinner of the household – maybe you’re a dual-income household, or maybe somebody else is the breadwinner – do you need mortgage protection?

Do you have investments you need to protect? Do you already have life insurance, but feel that you need more coverage?

What would happen if you/your spouse passed away tomorrow? Besides the obvious emotional heartbreak, the grief of losing your best friend, how would that affect you financially?

If you have a policy (or policies), do you understand how it/they would pay out? Does your policy have a delayed payment clause of any kind? If so, how long can it last? We’re on this side of the fence, and we’ve heard the horror stories – some people have had to wait months, sometimes half a year to receive their policy payout.

Does it exclude an unreasonable amount of “causes of death,” meaning it only pays out in specific situations? For example, some agents sell AD&D policies without telling their clients they only have coverage if they/their spouse dies as a result of an accident.

But the client is happy! Why? Because they “have” $100k worth of coverage for $35/mo. If it sounds too good to be true… It probably is.

If you add up everything you (two) own – your yearly salary, your investments, your debt, any large expenditures you plan on making, everything – do you have 7-10x that number in coverage?

But most importantly, do you know deep in your gut that you either need coverage, or more coverage than you currently have? Your subconscious mind is powerful, and it often “speaks” to us via “gut feelings.” You’ve had a supercomputer on your side this whole time and you didn’t even know it!

So if you feel, deep in your gut, that you need coverage/more coverage… Chances are, you do.

Pros and Cons of Traditional MPI

We’ve discussed how traditional MPI policies don’t hold a candle to how MPI works today. However, there are still some potential upsides to purchasing a traditional MPI policy with your lender.

Pros of Traditional MPI

~The Money Goes To The Bank

Now, I just got done talking about how this isn’t incredibly fantastic. Why would it suddenly be something you want?

There are some niche situations where this would be helpful.

For example, some families who aren’t very good with managing money. It can be difficult to prepare for and budget with a large sum of money that, in many cases, is supposed to last for a long time.

Many annuity products help with this issue, too – set somebody up with a single-payment immediate annuity (with their inheritance, lottery winnings, insurance payout, etc), and they receive a consistent paycheck instead of having one lump-sum of money that, quite frankly, can be handled irresponsibly at any given point in time.

But this only represents a small portion of our clients, and many of them can set up trusts and wills that direct where their family is to spend the money.

~Guaranteed Acceptance

While the premiums reflect this, you don’t have to go through an underwriting process to purchase this kind of policy. This can be appealing to many people, especially if they’ve been declined by life insurance companies in the past. (This usually isn’t a big deal, especially since we excel at finding solutions to difficult challenges.)

~Peace of Mind

You will have peace of mind that your mortgage is protected.

Cons of Traditional MPI

~The Money Goes To The Bank

For most families, this is a significant downside. Most families would benefit from having the money go to them, instead of the bank.

~Premiums Are Usually More Expensive

Either that, or you think you’re getting a good deal with a traditional MPI policy when in reality, it’s accidental-only.

~Coverage Declines While Payments Don’t

Remember, traditional MPI policies typically follow your mortgage – so if you start with a $200k mortgage, you’ll (likely) purchase a $200k policy. If you pass away when the mortgage is at $100k, only $100k pays out to the bank. If you pay for $200k in coverage, you/your family should receive $200k if/when the time comes, no?

~Greater Peace of Mind

Not only will you know that your mortgage is protected, but you’ll also know that the money is going to you/your family. After you/they pay off the mortgage, you/they get to keep the rest of the money.

And just between you and I, if something comes up before the mortgage is paid off, you can still take care of it. The insurance company isn’t going to come knocking on your door or anything like that.

Take care of business first and foremost, as much and as quickly as you can, and you/your family keep(s) the rest after the dust settles.

~Few Living Benefit Opportunities

Some TMPI policies offer a few benefits, like disability and “unemployment” riders. But these pale in comparison to the living benefits available to some clients with modern MPI policies.

Speaking of which…

Living Benefits

Modern MPI policies can offer living benefits, just like life insurance policies. A couple of LBs are usually included at no additional cost, depending on the company. Chief among these is the “terminal illness” (also called accelerated death benefit) rider, which allows the death benefit to be paid to you if you’re only given 12-24 months to live.

However, there are many other living benefits you may be able to qualify for. Keep in mind, the younger and healthier you are, the more likely you’ll be able to qualify for the following.

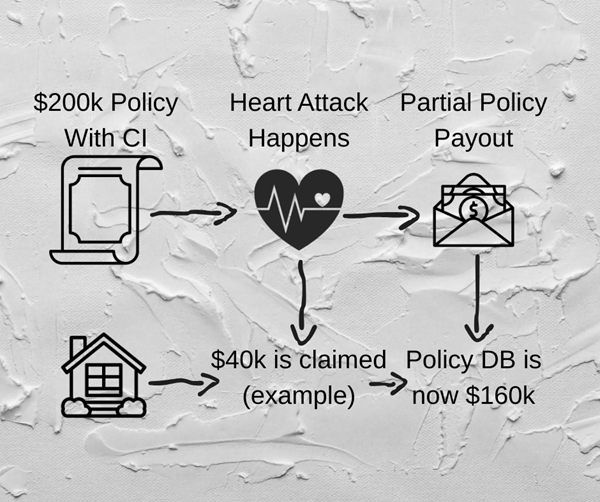

Critical Illness

In our opinion, Critical Illness (CI) is some of the most important coverage you could purchase today. Especially in America.

How it works is, if you suffer a “qualifying event” (such as a heart attack, stroke, cancer, and more), you get to pull out a percentage of the death benefit (usually up to 25%, 50%, or 100% of the DB) to use in any way you need to.

As we all know, medical bills can be incredibly expensive, and not everything is covered with health insurance. Have you ever looked through a BlueCross BlueShield summary of benefits? It’s kind of scary. At least with BCBS, a lot of things are covered after the $8,000+ out-of-pocket limit – but what if you don’t have BCBS and you’re required to pay co-insurance, if it’s even covered at all?

Heaven forbid something happens to you when you’re not in a covered state, for example.

Also, this doesn’t include any other bills you may fall behind on. We’ve had clients who were back to work in 6 weeks after suffering a heart attack. That’s great! But it also means he fell behind on all of his other bills too. It wasn’t a problem, though, because he was able to claim a check for $40k, more than covering all of his expenses, medical and otherwise.

To be honest, we’ve heard story after story after story, and it’s pretty definitive – even though this coverage costs you more per month, you’ll be very happy to have it if you need it, no matter where you are in life.

Disability Waiver of Premium

We usually just refer to this as ‘disability.’ What it does is protect your mortgage payments for up to 18 months if you’re unable to work due to a disability.

One thing we love about this rider is we’re contracted with companies that have “no-questions-asked” policies. Meaning, you can have as much work-provided disability as you’d like and it won’t affect your ability to qualify for disability through us.

Speaking of which, we highly encourage you to check your work disability coverage details. You may only have short-term disability through your job without even knowing it – again, we’ve heard the stories.

While this coverage is relatively inexpensive, it is a one-time use. It falls off after you claim the benefit for the first time.

Children’s WL and AD&D

While these are technically separate policies, we like to bundle these together with the “main” policy that protects you and your family. Reasons like this are why we’re more solution-minded instead of product-focused – we focus on meeting your needs instead of trying to find a singular “product” that’s supposed to solve everything.

Sometimes, we use AD&D as a part of our main strategy, but we’ll talk more about that in a bit.

Children’s WL (Whole Life) is incredibly inexpensive, and it provides two benefits to your children. One, it gives them what’s called a “certificate of guaranteed insurability.” Try saying that five times fast.

Insuring your children while they’re young means they’ll never be coming to us in their later years, potentially with a plethora of health complications, trying to purchase life insurance through us. Not even MPI, but life insurance, where the underwriting can be stricter.

Also, they have the ability to double their coverage with every life event, while still keeping that child’s rate. You can set each child’s coverage as low as $5k and as high as $50k, but $20k is generally a reasonable number to start with.

Why is that?

Well, they can double their coverage when they turn 25, when they get married, and when they buy their first home – so $20k → $40k → $80 → $160k, which is around the price of a modest mortgage.

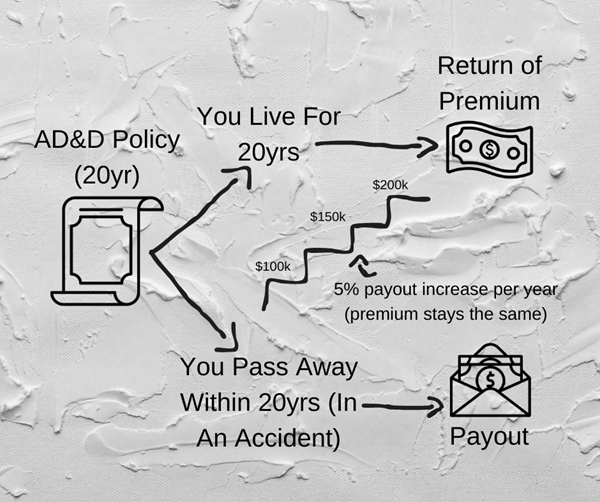

Now, I’ve been talking down on AD&D (Accidental Death and Dismemberment) policies throughout this post – why bring it up now? You know what they say, a picture is worth a thousand words:

Look at it again.

We have one particular company we’re partnered with who offers an AD&D policy that lasts 20 years. If you live the full 20 years, you get every dollar you’ve put into policy back in one lump-sum. If you pass away as a result of an accident, you obviously get a payout.

In addition, the payout increases by 5% every year, up until the policy expires at year 20. It starts at $100k. So, if you pass away as a result of an accident right after you purchase the policy, your family gets $100k. At year 10, that turns into $150k. At year 19 day 364, that turns into $200k.

And of course, the monthly premium stays the same.

You can’t lose when you purchase AD&D policies like this, as part of a package. If you bundle an AD&D policy with a policy that pays out no matter what, you’re going to either see a return of premium from your AD&D policy, a payout from your main policy, or from both your main and AD&D policies (if the cause of death is accidental).

You and/or your family will see money, whether you outlive the AD&D policy and get your money back, or if you/your spouse pass(es) away.

And the premium is relatively inexpensive.

Do you see why we like AD&D? It works for people, IF it’s implemented into a larger plan.

Return of Premium

Do you like the idea of getting your money back from the AD&D policy? How about everything?

If you qualify for Return of Premium (ROP), and if you don’t use your coverage in any way (no critical illness, no disability, and of course you don’t pass away), you get every dollar you put into the policy back in one lump sum (assuming it’s a term policy).

Some people really like the idea of receiving a payout no matter what. Not just for the AD&D policy, but for the entire package. If you’re going to see a payout no matter what, it’s easy to view insurance as an investment (legally, we have to say it isn’t) or at least, to have peace of mind that no matter what happens, you and/or your family will see something.

If you outlive a policy that has ROP, you can also tell the insurance company, “Keep the money and give me a reduced paid-up policy.”

What does that mean?

Essentially, the extra money you pay for ROP can be used to purchase a whole life (permanent) policy at the end of the policy term. It’s typically less coverage than what your term policy offered – however, you don’t pay anymore premium, and the payout is still worth more money than if you simply asked for it back.

You can also choose any combination in-between. At the end of your policy term, you can say “Hey, give me 50% of my money back, and keep the other 50% for a reduced paid-up policy.”

And the cool thing is, you don’t have to make that decision until the policy term expires. So, if you choose a 30 year term, you don’t have to make that decision for another 30 years.

Some people’s mantra is “term, and invest the rest.” They see ROP as unnecessary, because they have other investment accounts they want to build throughout their career(s). And that’s completely valid! ROP is an optional rider that you don’t have to add onto your policy, even if you qualify for it.

But, if you’re more in the camp of “money spent, money gone,” you don’t have much desire to invest, or you see reduced paid-up policies as a way of guaranteeing that you’ll “make” money on your money, ROP may work perfectly for you.

Other Living Benefits

Some livings benefits, depending on the company(ies) we write you with, may be included at no additional cost. These include long-term care and chronic illness.

Long-Term Care riders allow you to use some of your death benefit to cover long-term care expenses. Usually, your doctor has to provide documentation saying you need LTC that you would then give the insurance company.

Some of these expenses can include facility/nursing home fees (including home care fees), LTC healthcare fees, maybe even what you pay your friends/family for the care they provide you.

Chronic Illness Riders allow you to use some of your death benefit to cover expenses related to a diagnosed chronic illness.

Normally, a healthcare professional confirms that you cannot perform 2 out of the 6 daily living activities, and then you can give that documentation to the insurance company in the claims process.

How much money you receive from these riders depends on the company(ies) and policy(ies) we end up going with. While it’s usually not an extravagant amount, it’s still enough to be helpful in a time of need.

What About My Retirement Account(s)?

A lot of people don’t like insurance agents. I’m speaking about agents who sell life insurance, MPI, final expense, the kinds of policies that pay out after you pass away.

There are many reasons for this, but here’s what it tends to boil down to: They charge too much money, for too much coverage (or not enough), while potentially writing for companies who have a lot of “gotchas.”

Sometimes they lie, and sometimes they don’t have an understanding of the products they’re presenting.

But many agents simply aren’t aware of the bigger picture.

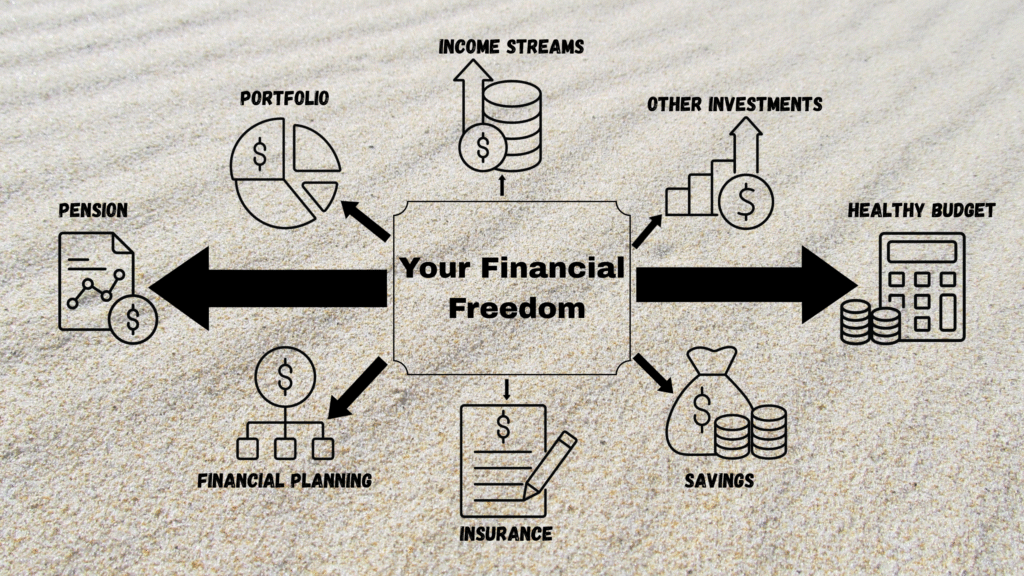

The bigger picture meaning your bigger picture. What your financial freedom looks like from a bird’s-eye view.

You may have an entire investing strategy. Maybe not, maybe you just have a 401(k), IRA, pension, HYSA, life insurance/final expense policy, Roth IRA, backdoor Roth IRA, or other investments.

And, life insurance/MPI might be your financial plan. This is true for some people, too.

But here’s my point – in a sense, insurance agents are often some of the last people to add value to your financial strategy. MPI is one piece in a well-orchestrated puzzle that’s meant to secure (and protect) your financial future.

Sure, MPI is better than nothing (trust me), but every single penny that you’re spending on insurance can be invested into your future. Or, simply enjoying yourself!

But, the reason why life insurance and MPI still holds so much prevalence is because of its protection.

Sure, you may have investment accounts, a beautiful home, and a rock-solid retirement plan – all you need to do is keep investing into it for a certain amount of time, and then you’re financially independent.

But what if you can’t do that anymore?

That’s what life insurance/MPI really is – it’s a safety net, a ward of protection against the unexpected. AKA, it’s one piece of your financial plan that’s meant to provide a solution to a niche situation. Just like how every one piece of your financial plan is meant to provide a solution to each of their niche situations.

Add everything together, and when implemented well, every component works together to create your financial independence.

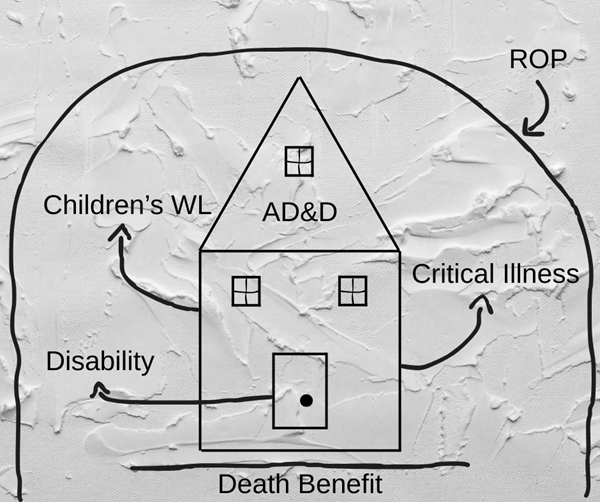

This picture sums it up pretty well:

Do you see why it doesn’t make a ton of sense to overcharge you and give you more coverage than you actually need? Insurance is just one part of a much bigger financial picture, and this is how we see it.

What If I Already Have A Policy?

If you have other insurance policies, whether owned by yourself or provided by your company, you may be wondering if it’s worth paying for multiple policies at the same time.

First things first, let’s talk about Evidence of Insurability (or EOI). When you apply for life insurance/MPI/final expense/etc, your EOI is being assessed by the company (or companies) you apply to.

Life insurance is primarily meant to be a financial safety net. It’s not meant to make you or your beneficiaries wealthy upon your passing. As such, they determine how much insurance you can have overall (across every company), based on a number of factors.

Some of those factors include income streams, how many assets you possess, your age, how much debt you have, etc.

For example, let’s say your EOI is determined to be at $1m. And let’s say that you already have a $700k life insurance policy.

Chances are, if you apply for an additional $450k in coverage, you’re going to be declined (even if you’re in perfect health) because you’re applying for more than what your pre-established EOI limit allows.

Auto insurance companies do something similar. If you have two auto insurance policies, and let’s say an accident occurs, the responsibility is split between the two companies (or between the two policies, if they’re with the same company). You won’t get a double-payout, but just enough to where you can pretend (financially speaking) that nothing ever happened.

This concept is called “indemnity.” That is, the insurance carrier’s responsibility to financially restore you to where you were before, as opposed to giving you money you never had prior to the incident.

Now, in our experience, most people don’t have to deal with this. 1, maybe 2 policies are usually enough to cover a family’s needs. But, it’s possible that you may not even be able to have multiple policies at a time, especially if you have considerable coverage with your current policy.

Let’s assume for a moment that you can; you have a $100k life insurance policy, and you’re interested in purchasing a $200k MPI policy for your mortgage. Is it worth it?

There’s one important distinction we have to make before answering this question – is your $100k life insurance policy with work? Or, do you own it outside of work?

There are many reasons why solely relying on company-provided life insurance is NOT a solid foundation for protecting you and your family. What if you pass away after you change jobs? Or after you retire? What if your company downsizes, resizes, restructures, and suddenly your benefits aren’t there for you anymore?

We count work-provided insurance coverage, we just don’t count on it. The question you want to ask yourself is, “Should I be putting the financial future of myself and my family entirely in the hands of my company?”

Can you truly, beyond a shadow of a doubt, prove that your company will always provide that coverage? And, can you prove beyond a shadow of a doubt that you’ll be working at that company on the day of your passing?

So far, no one has been able to say yes. And that’s ok! It just means that the financial security lies in owning life insurance/MPI outside of work, coverage that follows you wherever you go.

Theoretically, you could keep your company-provided life insurance (it’s usually very inexpensive, after all), purchase a MPI policy that you independently own, and be much more financially protected than if you didn’t.

But, okay – let’s assume you independently own your $100k life insurance policy. Is purchasing a separate MPI policy for your mortgage still worth doing?

Generally, yes, yes it is.

Now of course, that decision is ultimately up to you – worth and value are subjective, and you’re the only one who can decide how much value you place on protecting your possessions, and the ones you love.

But purely speaking from a financial perspective, the more coverage, the better. And, sometimes it’s cheaper to own two smaller policies than one larger policy. Sometimes it isn’t. That’s something you’d have to find out during the quoting process.

Again, if you don’t have coverage equal to or greater than 7-10x of everything put together (investments, debt, yearly salary, considerable future expenditures, etc), you may run the risk of being under-insured. There are other ways of calculating how much insurance you need, and Investopedia has a great article that dives deeper into these methods.

Now you may say, “That’s all well and good, but what if I can’t afford that much insurance?” And in reality, some people can’t. And that’s ok. One area where we shine is coming up with…

Creative Solutions

We use a couple of non-conventional solutions if it’s clear the underwriters are going to give us a hard time. It’s not my intention to offend anybody with this post, but you may have already been declined by an insurance company or two for various factors, including your age and/or your health. Or, the coverage you originally wanted was going to cost a small fortune for the same reason(s).

Maybe that’s even why you’re reading this post.

The reality of life insurance/MPI underwriting can be brutal, and that’s why we’ve committed to coming up with other solutions that work quite well. I’ll give you some examples.

Mortgage Payment Protection

Mortgage Payment Protection (also known as Critical Period Coverage) is a product that works a bit differently than what we’ve been discussing so far.

What we’ve been talking about up until this point is called Full Mortgage Payoff (or FMP). This is what most of us are familiar with when we think of mortgage protection – we think of a policy that pays off the mortgage if either you or your spouse passes away before the term ends.

But MPP is different in the sense that it allows the insurance company to take over your mortgage payments for a certain amount of time.

You decide how long that period of time is – many people choose 12 months, but we choose between a wide variety of increments (popular examples include 6, 9, 12, 18, and 24 months). In some exceptional cases, we’ve even had people apply for years (up to 10 last I heard) of mortgage payment protection coverage at a time!

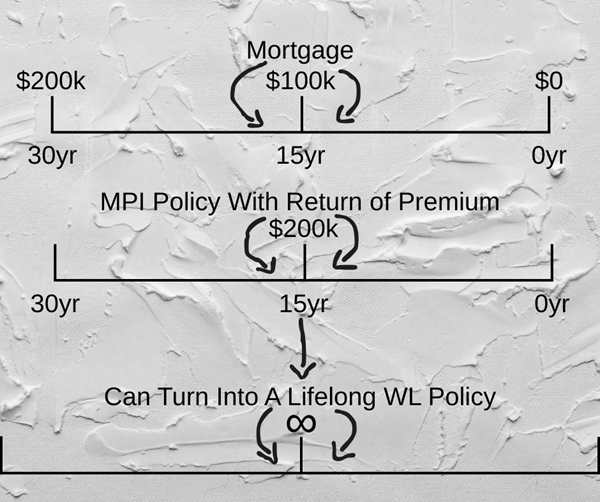

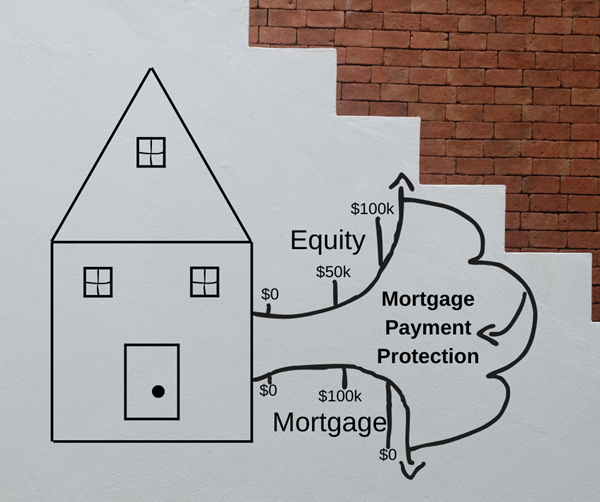

Additionally, we almost never rely on MPP by itself, but we use it as part of a strategy. Consider this graphic:

So, what are we looking at here?

On one hand, the value of your home is basically guaranteed to increase. Maybe not year by year – but over time, a home’s value will almost always end up being higher than your closing price.

Keep in mind, housing prices started rebounding only several years after the 2008 recession.

It’s also worth noting that, depending on whose graph you choose to look at, Covid-19 didn’t make housing prices go down – if anything, they increased during the brunt of the pandemic, only to start tapering off a tad in mid-2023.

Take a look at this graph, for example.

On the other hand, while housing (and land) prices keep going up (even after recessions and during global pandemics), what else keeps going down? Your mortgage. AKA, how much money will land in your pocket if you decide to sell the house.

If you buy a house on a $200k mortgage and sell it 15 years later when you’ve dropped it down to $100k, you’re able to pocket $100k more than if you sold the house 2 weeks after you bought it.

Many people also want to downsize if their spouse passes away before them. Maybe there’s too much upkeep, too many memories, they want to move closer to their kids, or even move in with their kids. And if not, there’s always the possibility you can re-finance (or recast your loan) if need be.

Either way, here’s our strategy: Why not see your ever-increasing equity as an increasing death benefit that’s complimented by your ever-decreasing mortgage? Counting on an arrangement that you’ve already set up, but that needs to be protected until you can get your affairs in order?

After all, if you/your spouse pass(es) away, the bank doesn’t want the entire mortgage all at once, do they? No, of course not – they just want the next payment.

Even having 6 months of mortgage payments taken care of for you (we recommend at least 12) can mean the difference between everything transitioning smoothly, and chaos. There are plenty of nightmare stories out there, trust me.

Underwriting guidelines are already reduced with MPI policies because you own a home, but even more-so with MPP policies. It’s also very common for people to be able to afford these kinds of policies, even in their later years, and even on a fixed income.

While you may not qualify for living benefits with this type of policy, it is a permanent policy, meaning it’s guaranteed to pay out to you and/or your spouse. And when the time comes to use it, you’ll be able to buy yourself enough time to sell the house, re-finance/recast your loan, liquidate some of your assets, or whatever you need to do to make it through, without having any fear of the bank re-possessing your home.

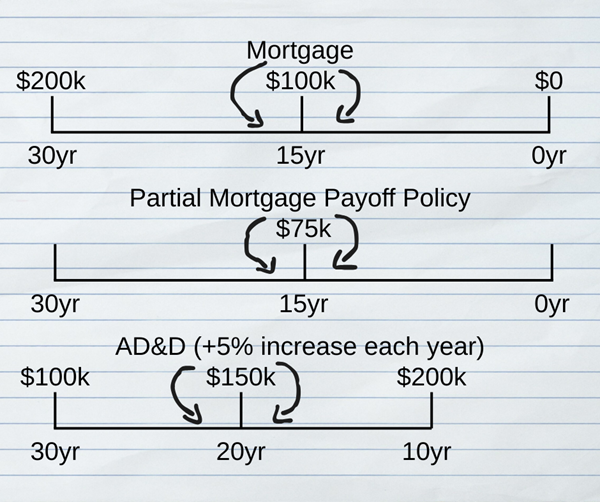

Partial Mortgage Payoff With AD&D

Picture this – you’re a couple in your mid-50s. You’re both on a couple of medications, but your medical history isn’t complicated by any means. You just took out a $200k mortgage and you’re moving into your brand new home.

…And then you find out that a Full Mortgage Payoff (FMP) policy is going to cost you $400+/mo. Each. Yikes.

You’ve decided that you don’t want a MPP policy, and that you’d rather cover the full amount of the mortgage. But you may feel that your back is up against the wall. What do you do?

Instead of just writing you a Partial Mortgage Payoff policy (which, granted, some people want to go down that route), we have another strategy that looks like this:

Here’s the logic: The AD&D policy lasts for 20 years. Once you turn 60, we can’t write you an AD&D policy anymore. And, the main breadwinner(s) of the home is/are likely still working.

So, why not give you a partial mortgage payoff policy that pays out no matter what, and layer an AD&D policy on top of it?

After all, you’re less likely to die from an illness and more likely to die as a result of an accident in the next 20 years. If that happens, then you receive a minimum of $100k from your AD&D policy (remember, the payout increases by 5% each year it’s in place), and whatever amount from the partial mortgage payoff policy. Let’s call it $75k.

And the best part about this strategy? It’s affordable for so many families.

In our example, you’re still pretty healthy in your 50s, which a lot of people are. If you aren’t, no worries – worst case scenario, the partial mortgage policy pays out and the money still goes to your family, so they get to use it however they’d like.

If you want to pay your monthly mortgage payments while you adjust (instead of a lump-sum payment to your lender), you’re more than welcome to do so. This way, you wouldn’t be financially strapped while your house is on the market, for example.

Depending on where you’re at, you may be able to pay off part of the mortgage, and refinance/recast your loan to lower the monthly payment. Sometimes this can help, and sometimes it doesn’t do much – again, it depends on where you are at that time. At the very least, you’d be able to avoid paying some interest if you went down this path.

But this is the worst case scenario – the chance that you’ll/they’ll live 20 additional years and get ROP on your AD&D policy is higher than 0. The chance that you’d/they’d die as a result of an accident instead of health-related issues (unless you/they currently have something) is likely high as well.

Is this a perfect strategy? No, of course not. Some people don’t qualify for AD&D because they have a “hazardous job,” or because they’re over 60 years old. Sometimes we have to set them up with a standalone partial mortgage payoff policy, and/or an MPP policy.

But it’s a heck of a lot better than nothing, that’s for sure.

Exploring Alternative Policies & Policy Combinations

Short of giving you a piece of scratch paper and calling it your policy, we’re willing to go to great lengths to forge a solution for you and your family. As such, we have access to other kinds of policies that can be helpful in very specific situations.

We generally try to avoid using these types of policies because of their glaring drawbacks. For example, policies with a “graded death benefit” won’t pay the full benefit if you die within the first two years of owning the policy (unless you pass away as a result of an accident). Instead, you’d receive a return of premium plus interest. Then, starting on year 3, 100% of the death benefit would pay out to you/your family.

The upsides to these kinds of policies, however, may include reduced premiums and/or more relaxed underwriting requirements.

If you’re below age 60, we can bundle an AD&D policy along with your graded death benefit. Another option is bundling a graded death benefit policy with an MPP policy – at that point, you’d have coverage no matter when you/your spouse pass(es) away.

Or, perhaps we can bundle all 3, if the budget permits.

Another alternative is a “Guaranteed Issue” policy. These policies, as the name suggests, are guaranteed to be issued to you regardless of your age or health.

Your EOI limit may still prevent you from purchasing a “guaranteed issue” policy, but if you’re concerned about that, you probably already have an abundance of coverage.

Guaranteed issue (GI) policies typically have a graded death benefit as well. The difference between GI policies and regular graded death benefit policies is that GI policies typically have a relatively low cap in how much coverage you can purchase, usually $25k-$50k. They can also be more expensive than regular policies.

And of course, they’re guaranteed to be issued.

A GI policy could potentially work if you were originally looking for a Mortgage Payment Protection-esque solution, but you couldn’t qualify for one. (And if you were looking for an MPP-esque solution, chances are you couldn’t qualify for full/partial mortgage payoff.) In most cases, you could still apply for 12 months of mortgage payment protection with a GI policy, giving you enough time to get back on your feet if something were to happen.

Some of these policies have a negative connotation surrounding them. That’s possibly because some companies try to sell you these kinds of policies, claiming that they’re greater than we really are…

But if we have to choose one of these options, we’re honest about the pros and cons, and the reasons why we’re presenting them to you. Full transparency and honesty is a core part of who we are.

And often, we’ll come prepared with multiple options. So for example, if we show you a graded policy and it makes your skin crawl, we’ll show you options for partial mortgage payoff + AD&D, MPP + AD&D, AD&D standalone (which we really try and avoid), or whatever we think you’ll qualify for (that meets your/your family’s needs, of course).

If we suspect we’ll have to come up with some creative solutions, we like discussing them with you over the phone before we even set the appointment – but even still, some of them can be daunting to look at in the moment, and we know that.

That’s one of the reasons why we come prepared.

So, why did I list all of these examples, anyway?

To prove a point – that being, we’re truly committed to finding out what your needs are, and taking care of them to the full extent of our power. Sure, sometimes we’re limited by what the underwriters tell us, and budget constraints are the norm rather than the exception.

But, we’re willing to work within these parameters and do our very best to overcome every challenge that comes our way – as corny as that sounds to me reading it back.

Conclusion

Mortgage protection is a lot more than it used to be. Before, you would simply add it onto your mortgage payment. But nowadays, there are so many options and benefits you could potentially choose from. It can feel a bit overwhelming to say the least.

That’s why we’re here to guide you, consult you, and use our expertise to find the solution that best fits your/your family’s needs. And on top of that, maybe give you some extra benefits!

If you’ve read this far, you’re probably interested in seeing what we have to offer. Click here to get your quote started today!

Copyright © 2025 www.mohrprotection.com. All Rights Reserved.